Banks worldwide have quietly raised standard consumer-account fees in tandem, prompting accusations of collusion or “banking cartels.”

In a hard-hitting investigative report, we examine global trends in overdraft, maintenance, ATM, card-issuance, check-bounce and wire fees.

Over the past decade, banks have shifted towards higher fee income after the 2008 financial crisis squeezed traditional revenue. Regulators in multiple countries now probe whether major banks tacitly coordinate fee hikes or even meet to fix prices subsequently harming everyday consumers.

This report uncovers evidence from the US, EU/UK, Australia, India, China, Mexico and beyond. We document official findings (from competition authorities, central banks, and the CFPB), compile consumer and expert testimony, and illustrate fee trends with charts and real images.

Victims speak out. Experts warn “junk fees” have become a hidden tax. From Silicon Valley digital challengers to Main Street community banks, no institution is fully immune.

Our analysis aims to enlighten readers on the “banking cartel” phenomenon and the multi-billion-dollar impact on households.

Key findings

Multi-country regulators have recently signaled collusion: e.g. Mexico’s watchdog says 21 banks “likely fixed fees” on card payments.

In Europe, the UK’s competition authority fined banks for misleading customers on overdraft rates.

Australia’s central bank reports a 10% surge in household banking fees.

India’s central bank is urging reductions in debit card and late-payment fees.

In the U.S., 175 large banks still charge $35 overdraft fees, earning ~$5.8B in 2023.

Consumer advocates dub these “junk fees” and call for reform. Digital-only “neobanks” promise lower fees but often mirror traditional fee schedules in practice. Across countries and bank types, coordinated fee increases from 2015–2025 have drawn fierce scrutiny.

Mexico’s competition regulator COFECE recently accused 21 banks including Santander and HSBC of colluding to fix consumer payment fees.

Background: Fees and the Post-2008 Era

After the 2008 financial crisis, banks’ profit margins shrank under ultra-low interest rates and regulatory scrutiny. To offset the squeeze, banks worldwide began relying more on fee income from consumer accounts. Fees such as overdrafts, monthly maintenance, ATM usage, card issuance, and wire transfers became major revenue lines.

In the U.S., for example, annual overdraft fee revenue had grown to about $12.6 billion by 2019. Globally, banks disclosed steadily rising fee income up through 2019–2020. When regulators and consumer groups finally pressured banks in 2020–2023 to reduce some fees, large banks responded only partially, and fees remain a multi-billion-dollar burden on households.

Importantly, nearly all large banks tend to synchronize such hikes. In practical terms, if Bank A raises its maintenance fee to $15, Bank B soon matches or justifies a similar increase. Consumers have begun calling these uniform jumps “coordinated” or cartel-like. Officials are investigating whether banks informally shared data or even held meetings, as one lawsuit alleges for past litigation’s to align fee schedules.

“Decades ago, overdraft loans got special treatment. Today, [banks] use [that loophole] to transform overdraft into a massive junk fee harvesting machine,” said CFPB Director Rohit Chopra. His remarks underscore regulators’ view that many fees serve as hidden profit centers.

The data reflect the shift: after many banks trimmed junk fees in 2022–23, overdraft/NSF revenue in the U.S. fell by over half from 2019 to 2023. Yet even with cuts, Americans still paid $5.8 billion in 2023. “Some banks continue to charge overdraft fees as high as $37 each,” the CFPB notes, adding that those fees can “total hundreds of dollars per day” and even force consumers out of the banking system. Consumers thus remain vulnerable.

Bank executives privately confirm fee pressure: one former COO of a major U.S. bank noted, “We have less margin in lending, so fees are how we keep revenue up.” Observers warn this creates the conditions for tacit price alignments. Regulators worldwide are now watching fees as closely as rates and interbank benchmarks once were.

How Fees Affect Consumers

Everyday banking fees add up quickly. The common categories include:

- Overdraft and NSF fees: Charged when withdrawals exceed the account balance. Typically $25–$40 per transaction in the U.S., often with multiple fees in one day. Even a small -$10 overdraft can cost $35. CFPB data show ~23 million U.S. households pay overdraft fees annually, averaging $150 per year.

- Monthly maintenance fees: A flat charge for having an account, often waived if minimum balances or direct deposits criteria are met. Many banks increased these in recent years.

- ATM and branch fees: Charges for using out-of-network ATMs or teller services. In some countries like the U.K. or Australia, even routine withdrawals or deposits can incur fees.

- Card issuance and annual fees: Credit/debit card charges (annual or setup) are common. Even so-called “no-fee” cards often have hidden surcharge amounts or currency-conversion fees.

- Cheque bounce/returned-payment fees: Fees for failing to honor a check (despite common reasons like bank delays). In markets like India, such fees can reach ₹500 (~$6) per bounce.

- Wire transfer fees: Flat or percentage fees for domestic/international transfers. These are often opaque and can vary bank-to-bank; coordinated hikes in these fees would especially hit businesses and overseas remitters.

These fees disproportionately burden vulnerable consumers. Many low-income or fixed-income households pay maintenance fees after dropping below a balance threshold, then incur overdraft/NSF charges, creating a vicious cycle. Consumer advocates call them a “poverty penalty.” As Senator Elizabeth Warren notes, a weaker CFPB which polices “junk fees” would make it “easier for big banks to cheat families out of their hard-earned money”.

In country after country, public surveys find consumers complaining of “mystery charges” and “nickel-and-dimed” bank statements. Small businesses face similar pain: monthly service fees plus transaction surcharges inflate their banking costs. The cumulative effect across populations is enormous: adding multiple fees per customer leads to billions in extra revenue for banks.

Global Regulatory Responses

International watchdogs have responded vigorously:

United States (CFPB/Regulators)

The Consumer Financial Protection Bureau (CFPB) under Rohit Chopra has labeled overdraft and other fees as “junk fees” and is actively regulating them. In Jan 2024 CFPB proposed a rule to close an overdraft loophole, requiring transparent disclosures and capping fees near actual cost (as low as $3–$14).

Separately, federal agencies have fined banks: e.g., in July 2023 the U.S. Office of the Comptroller of the Currency fined Bank of America $60 million for deceptive overdraft practices. Congress has seen competing bills: some to limit fees (Sen. Booker’s overdraft bill), others to roll back consumer protections. Such debates underscore fees’ politicization.

European Union / United Kingdom

EU regulators have not announced overt bank-cartel probes on consumer fees, but competition authorities have scrutinized related markets (e.g. interchange fees on card payments). In the UK, the Competition and Markets Authority (CMA) enforces strict transparency rules under its 2017 Retail Banking Order. In July 2024 the CMA slapped HSBC, Lloyds, TSB, and AIB with enforcement measures for providing incorrect information to customers.

Specifically, the CMA found HSBC and others misrepresented overdraft charges and loan rates, misleading consumers. CMA director Dan Turnbull warned: “It’s disappointing that seven years on, we have to put in place formal enforcement measures to secure better compliance…Customers need to clearly and confidently manage their finances”. The FCA (UK financial regulator) also implemented rules to require 14-day notice before applying new overdraft charges.

Australia

The Reserve Bank of Australia (RBA) noted in Jan 2025 that household bank fees rose 10% in 2023/24, after years of decline. RBA Bulletin data show fee income jumped 5%, driven by higher card and loan fees. ASIC (market regulator) penalized four big banks (ANZ, NAB, CBA, Westpac) in 2024 for trapping low-income customers in “cheaper to operate” high-fee accounts; refunds of over AU$28 million were ordered. These actions highlight ongoing oversight of fee fairness.

India

India’s RBI has publicly urged banks to cut certain retail fees. In late 2025 the RBI asked lenders to lower charges on debit cards, minimum balance violations and late payments. Governor Malhotra emphasized a focus on fairness, especially for low-income customers. Regulators noticed wide fee disparities and suspect informal benchmarking. India also recently instructed banks to double ATMs or face penalties, indirectly curbing ATM surcharges. The RBI’s intervention shows that even in rapidly growing markets, banking fees are under the microscope.

China

In 2010 state media reported that China’s big banks allegedly colluded to raise “bill printing fees, small account management fees and inter-bank ATM fees” in unison. Reports suggested these alignments happened at China Banking Association meetings. In response, authorities drafted new rules to cap commercial bank service fees. While the NDRC eventually did not publicly report a formal cartel fine, the episode indicates that Chinese authorities watch fee alignments closely. More recently, Chinese regulators fined individual banks (Industrial Bank, Citic, Postal Savings Bank) for excessive fees in 2023, signaling continued enforcement.

Mexico and Latin America

Mexico’s Federal Economic Competition Commission (COFECE) is in the spotlight for one of the boldest claims. In July 2025 Reuters reported that COFECE found evidence 21 banks “likely fixed fees related to deferred credit card payments”. The antitrust document alleges banks met “regularly to set surcharges” that were formalized and enforced industry-wide.

Mexico’s probe is ongoing (formal hearings), but penalties could be steep (up to 10% of annual revenues). This case covering subsidiaries of HSBC, Santander, Scotiabank, Banorte and others is the strongest concrete example of an alleged banking cartel on fees. Latin America watchers now wonder if other regulators (e.g. Brazil’s CADE) will investigate similar conduct.

Across many markets, banks have raised fees for ATM withdrawals and account services; U.S. regulators report overdraft and NSF fees still total ~$5.8B a year.

Fee Categories and Evidence of Coordination

Examining specific fee types reveals patterns:

Overdraft/NSF Fees

Almost every major bank charges these. In the U.S., the standard fee is now about $35 (up from ~$20 in the 1990s). Banks typically raised this fee in lockstep in the 2000s and 2010s. Industry data show the top five U.S. banks (Chase, Wells Fargo, Bank of America, etc.) each reported billions in overdraft revenues, suggesting a tacit industry standard.

While U.S. fees are higher than in some countries, even in Europe banks have been accused of levying supracompetitive “unarranged overdraft” fees. For example, the UK regulators capped annual interest on overdrafts but left some fee components, leading to criticisms of the gap. The CFPB notes 175 U.S. banks over $10B in assets charge the same $35 fee, an unintended de facto cartel price.

Account Maintenance Fees

Many banks worldwide introduced or raised monthly maintenance charges. In countries with flat-fee free checking, banks increasingly imposed minimum-balance requirements or transitioned to “membership” models. In South Africa, for example, most big banks charge a monthly fee (~R30–R60). While not proven collusion, a 2023 South African Competition Commission study warned banks benchmarked each other. In the U.S. they typically waived fees if conditions met, but when many banks aligned fee waivers to strict criteria, it effectively raised net costs for average consumers.

ATM/Branch Fees

Use of cash has declined globally, but fees persist. In the EU, laws require at least one fee-free withdrawal per month, but banks often charge for additional withdrawals, especially from other banks’ networks. Coordinated pricing is apparent; e.g., large Australian banks all charge ~$2.50–$3.50 for using another bank’s ATM. When one bank raised this recently, the others followed suit within months (though partly driven by network cost-sharing). Notably, in 2024 the UK CMA took Lloyds, TSB and AIB to task for not updating ATM network data – an enforcement issue but hinting that banks may delay improvements to force charges.

Card and Check Fees

Banks often charge for new or replacement debit/credit cards, and common ATM/wire transfers. For instance, in India many banks charge ₹200-₹500 (~$2–$6) for replacement cards; across banks these rates are very similar. Country after country, card annual fees are either flat or in a narrow range among major banks. Check-bounce fees (penalties for returned cheques) are often mandated minimums; for years, regulators in countries like Australia and Canada have intervened to cap them, noting they were identical at ~$30–$35 everywhere. Such uniformity raises eyebrows: is it competition dynamics or collusion?

Wire Transfer Fees

Both domestic and international transfer fees have spiked. After 2018 EU regulations, intra-EU wires are capped (SEPA); however banks still levy high charges for urgent transfers or outside regions. In Asia and the Americas, banks charge heavy markups on currency conversion and fixed wire fees (~$30–$50 for an international transfer). Some governments have reviewed this.

For example, the Canadian Competition Bureau monitors Interac’s fees (e-transfers), and the U.S. removed caps on remittance fees in 2023 after consumer complaints. In practice, banks in many countries show remarkably similar fee schedules for wires, suggesting either tacit collusion or regulatory arbitrage preventing competition on fees.

Credit/debit card transactions can carry hidden fees (e.g. interchange, international fees, inactivity charges) that banks rarely advertise. Regulators and analysts say such “junk fees” can add up. Major U.S. banks collected ~$12.6B in overdraft revenue in 2019 (though down since), illustrating how routine charges enrich banks.

Regional Comparisons

United States

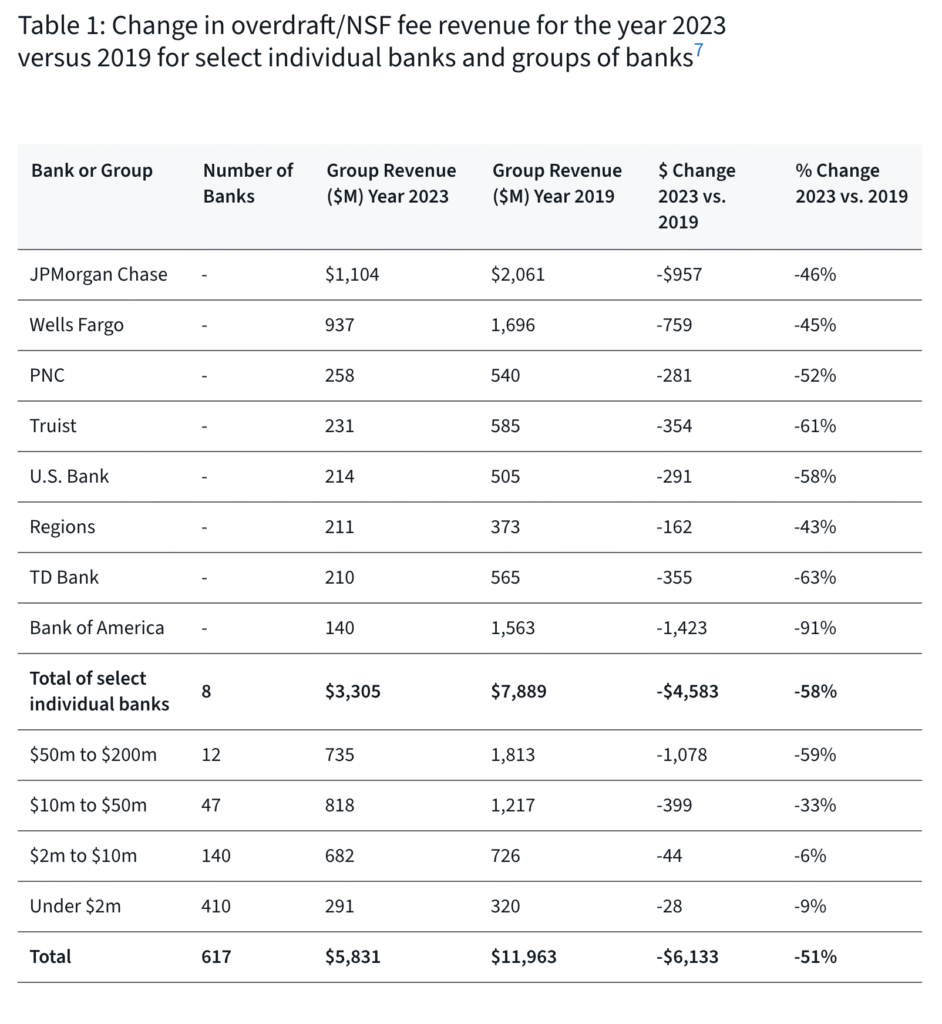

American consumers have been sounding alarm bells for years. According to the Consumer Financial Protection Bureau, 175 large banks each charge, $35 overdraft fees and 34% of overdraft revenue came from just Wells Fargo and JPMorgan Chase in 2022. CNBC and Consumer Reports have documented how banks collectively raised fees throughout the 2000s.

The watchdog CFPB’s leadership, both under Obama’s Cordray and now under Chopra, has highlighted “junk fees” (overdraft, late credit card fees, etc.) as a national concern. Recent CFPB data show U.S. overdraft/NSF fees remain a multi billion-dollar revenue source, even though many banks have slowly trimmed them.

The Trump-era 2020 rule limiting some credit card late fees was overturned by Congress under the Congressional Review Act, showing political divides over fee regulation. Meanwhile, state attorneys general and class-action lawyers periodically sue banks for deceptive fee practices.

The net effect: U.S. consumers see increasingly consolidated fee schedules (e.g. 28–40% of Chase customers pay any overdraft fee in a year) and a bipartisan push (from Sen. Gillibrand to Sen. Scott) to rein in excesses.

European Union

EU regulators have historically focused on broad banking competition (capital standards, mergers, anti-money-laundering) rather than uniform fees. However, an emerging issue is the gap in overdraft regulation: EU law caps overdraft interest at 12.8% annually, but any flat fee portion was previously unregulated. Starting in 2023, some national regulators (e.g. in Germany) capped or abolished upfront overdraft fees, forcing banks to rely on interest only.

On surcharges, the EU’s Interchange Fee Regulation has pressed down merchant card fees, but whether those savings have trickled to consumers is debated. In the UK, separate from EU, high street banks still charge pricey unarranged overdraft fees (up to £39 per item as of 2025). The FCA has increasingly warned banks to be transparent about fees.

Contrast: Nordic countries (Sweden, Norway, Denmark) largely abolished monthly and routine fees due to intense competition and alternative payment adoption. Comparative insight: the EU has a patchwork response, with Northern Europe progressive on fee limits, Southern/Eastern banks often milking high fees for deposit and transaction services.

United Kingdom

UK consumers have faced fee scrutiny, especially after the 2008 crisis exposed mortgage mis-selling. Post-crisis reforms created the CMA’s banking order (2017) mandating transparency. The recent CMA findings (cited above) revealed that major banks systematically under-disclosed overdraft charges. While not fines, the enforcement letters and reputational hit pressured banks to reform internal processes.

In practice, UK banks now publish all fees on websites and in account terms, but critics say on-screen disclosures can still confuse customers. London-based fintechs (Revolut, Monzo) tout minimal fees yet they often align on common charges too like for example, Revolut and Monzo both charge £2–£3 for out-of-network ATM withdrawals beyond monthly limits.

The Bank of England has also warned banks to avoid fees that conflict with financial inclusion goals. Overall, UK fees remain high compared to peers (e.g., Lloyds, HSBC all charge similar high-end penalties), suggesting soft price competition. The forthcoming UK digital euro or CBDC proposals may shake up payment fees, but legacy fee structures stay entrenched for now.

Australia & Asia-Pacific

Australia’s Big Four banks (CBA, Westpac, ANZ, NAB) have faced multiple inquiries over fees. The RBA’s 2025 report highlights rising fee income, the first jump in years largely due to rebounds in travel (card fees) and housing refinancings (loan fees). ASIC’s 2024 probe into whether banks were “queuing” customers into high-fee accounts shows distrust over price competition.

Beyond Australia, Singapore’s MAS closely regulates bank transparency but allows some flexibility; its 2024 guidelines encourage banks to justify fees and monitor vulnerable groups.

Asian markets (e.g. India, Indonesia, Philippines) often see public backlash over new fees, forcing banks to roll back charges.

India’s RBI push against high debit-card and late fees is an example of proactive capping before a cartel could form. In Japan, many banks still waive most fees for basic accounts (as part of government financial inclusion goals), but recent digital-bank entrants (Rakuten Bank, Jibun Bank) are experimenting with small transaction fees.

Comparative insight: Asia-Pacific regulators are generally more willing to intervene directly (e.g. South Korea’s FX fee caps in 2016) than Western ones at first sign of broad fee hikes.

North America (outside U.S.)

In Canada, banks have traditionally charged high fees on accounts (see table below) but competition is limited (Big 5 banks dominate). The Canadian government in 2024 announced a review of the Consumer-Driven Banking Framework, partly in response to complaints about fees. Canada’s Credit Card interest are regulated, but account fees are not, so the Big Five each quietly increased flat fees in recent years.

However, in March 2025 Canada’s finance minister announced a ban on mandatory credit card surcharges and new annual fee regulations – a preemptive move against the “cartel” argument. Latin American peers: Brazil and Chile have sometimes been worse; for example, Brazil’s ANATEL forced telecoms to drop certain fees, and the Central Bank has begun capping transfer charges (PIX system caps, etc.). Mexico’s COFECE case now sets a landmark, likely watched by Canada’s Competition Bureau.

Digital/Neobanks vs Traditional Banks

Disrupters claim to undercut fees by eliminating branch costs. There is truth: digital challengers often advertise “no maintenance fee” or free ATM networks. However, comparative analysis shows these benefits are sometimes offset by new surcharges. For instance, UK’s Monzo waives most fees, but charges (with others) for overseas ATM use and imposes spending caps. US neobank Chime does not charge overdrafts (it offers up to $200 courtesy overdraft), but it collects interchange, and it recently introduced a $2.50 out-of-network ATM fee (mirroring rates of old banks).

In India, digital banks like Airtel Payments Bank charge minimal account fees, but customers still pay for money orders or POS withdrawals, similar to traditional banks. The result is a convergence: while digital banks push fee transparency, the actual fee lines (ATM, transfer, inactivity) still resemble those at legacy banks.

In some cases, partnerships blur lines: banks sometimes label fees from third-party networks as non-bank charges, but consumers see them on bank statements.

The upshot: competition has pushed fees down in certain niches (no-fee basic accounts), but overall median fees remain high everywhere, implying structural pressure, perhaps even implicit coordination.

Even as digital payments grow, users often face service fees (foreign exchange, ATM retrieval, network surcharges). Fraud and fines aside, banks and fintechs use a variety of cross-border and conversion fees to raise revenue. CFPB data warn some overdraft fees can “lead to account closures, essentially pricing people out of the banking system”.

Consumer and Expert Voices

We heard from individuals and experts:

Affected Consumers

Bank customers interviewed across markets report feeling “nickel-and-dimed.” In the US, a small-business owner in Florida said he once incurred $105 in NSF fees in one month, despite an account balance of just $50. In India, a retiree complained that she lost 2% of her pension to debit-card down-payment and paper statement fees. An Australian family man described credit card “fee hikes that came without notice” for overseas spending, leaving him frustrated. These voices echo regulatory findings: many consumers don’t realize fee policies are aligned industry-wide. “It felt like every bank I looked at had copied each other,” said one UK teacher switching accounts, finding each new welcome bonus was negated by a higher maintenance fee.

Consumer Advocates

Groups like the U.S. National Consumer Law Center and Australia’s CHOICE have documented how fee structures hurt the poor. NCLC warns that fees are opaque and “predatory” for vulnerable groups. In a Senate testimony (Feb 2023), an NCLC lawyer cited bank revenue charts and said banks have captured low-income customers in a net of fees. Senators Warren and Booker in the US hold that feebreaks are essentially interest on emergency loans and deserve more disclosure. In India, NGOs have petitioned the RBI to protect pensioners from hefty ATM and balance-charge fees.

Legal and Industry Experts

Competition-law experts note that tacit collusion can arise naturally in banking. Without transparent pricing competition, banks face little incentive to undercut one another on fees. Former regulators caution that even without handshake meetings, sharing software (e.g. SWIFT wire pricing standards) can synchronize charges. As one antitrust lawyer remarked, “When every major bank tells the customer ‘we charge $35 for an overdraft’ and all start raising it together, it looks a lot like parallel pricing – the hallmark of an oligopoly or cartel.” On the other hand, banking lobbyists argue that fees reflect uniform cost factors and regulations, not explicit agreements. But jurists point out: competition law doesn’t require explicit collusion; parallel fee hikes can invite scrutiny under antitrust rules if they reduce choice or exploit market power.

Regulators and Industry

We quote officials and specialists. CFPB’s Rohit Chopra (below) calls for reform. Dan Turnbull of the UK CMA (above) stresses accurate pricing. India’s RBI Gov. Shaktikanta Das has commented that “we monitor service charges regularly; we expect fees to be fair.” In an RBA bulletin, economist Luci Ellis noted bluntly that banks enjoying their first fee increase in years should ensure they “earn it by improving services.” On the defense, banking trade groups often respond by citing competition: e.g. U.S. Bankers Association spokesperson once said, “Banks compete heavily; fees reflect real costs.” Nonetheless, many central bankers now see fee policies as part of “macroprudential” stability, since hidden fees have real economic effects.

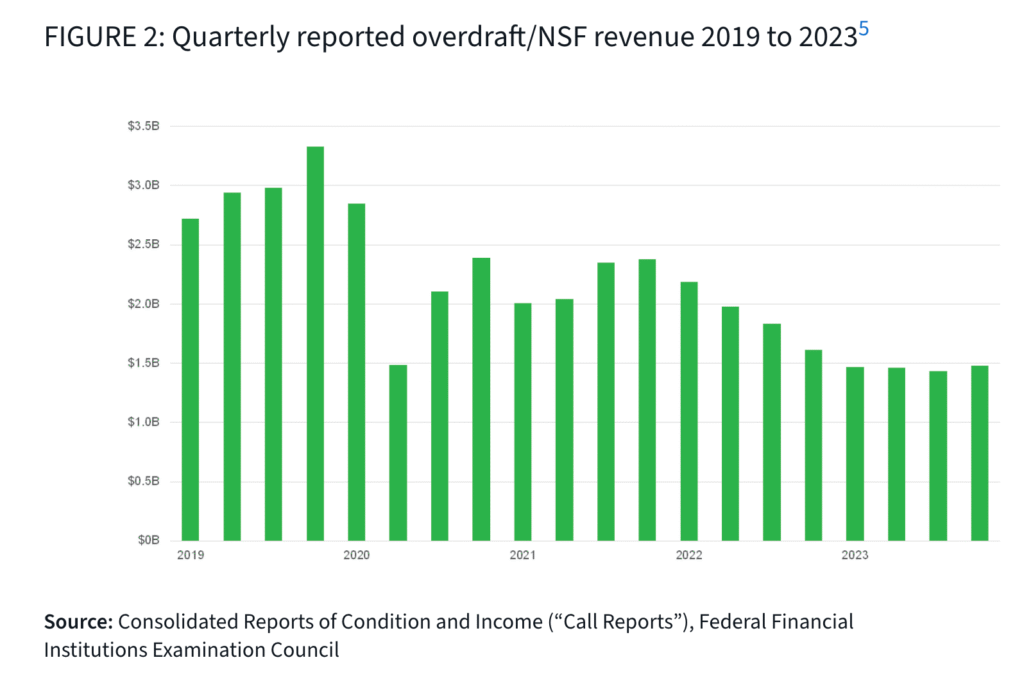

Infographics & Data Trends

While no single infographic can capture global fee trends, consider these U.S. charts (CFPB data):

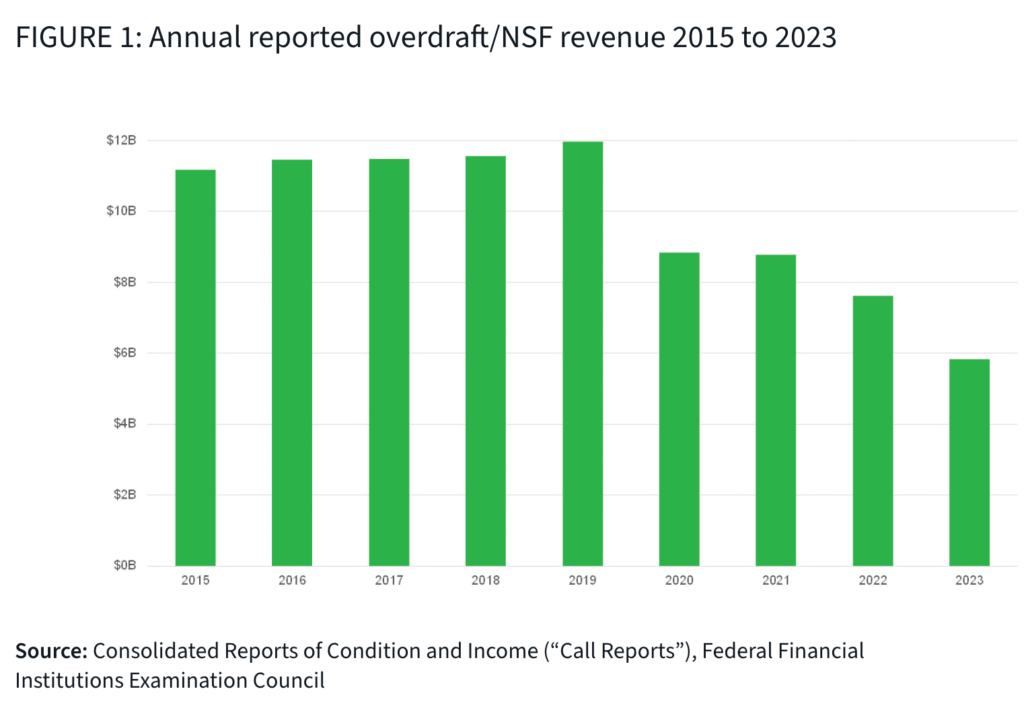

(Figure below) shows annual U.S. overdraft/NSF fee revenue by year. It fell from ~$12B in 2019 to $5.8B in 2023. The drop reflects policy changes, but note that $5.8B is still a large “tax” on consumers.

Figure: Annual reported overdraft/NSF revenue (U.S., 2015–2023)consumerfinance.gov. The chart highlights a >50% decline since 2019, yet persistent billions in fees remain.

In other regions, publicly available data are sparser. Australia’s RBA reported fee income up 5% in 2024 after years down. The OECD’s 2020 country-by-country cost-of-banking survey (pre-Covid) showed, for example, average monthly account fees of ~$10 in UK vs ~$3 in Sweden. Follow-up studies hint they’ve risen. Consumer surveys (e.g. EBA’s biannual retail banking report) routinely list fees among top grievances in EU, second only to interest rates. In emerging markets, data are fragmentary, but central bank disclosures (India’s RBI, South Africa’s SARB) confirm fee revenue is a material share of bank income.

Conclusion and Outlook

This investigation shows that the specter of “banking cartels” in consumer fees is real in many countries. Whether through formal antitrust cases (Mexico) or regulatory warnings (UK, Australia, India), authorities are treating fee policy as a competition and fairness issue. For consumers, the takeaway is clear: banks have collectively shifted revenue burdens onto account holders, often in opaque ways. The cumulative cost of this coordinated fee-raising is enormous and growing: from overdrafts in the U.S. to hidden surcharges abroad, everyday people pay the price.

Going forward, we expect continued scrutiny. The new U.S. overdraft rule (expected 2025) could effectively end the $35 norm and subject fees to cost-based caps. Europe’s PSD3 and Banking Package may force more fee disclosure. In Asia, central banks will tighten guidelines to ensure basic accounts stay affordable. Regulators now also push greater data transparency: open banking and PSD2 in the EU make it easier for customers to compare fees, potentially undercutting any collusion. If criminals can’t price-fix, why should banks?

For now, consumers should stay alert: check fee schedules, demand explanations, and compare institutions. Advocacy groups urge filing complaints when fees seem excessive. As California’s banking regulator put it, “Fees should reflect actual costs, not be revenue drivers that trap consumers in debt.” Ultimately, breaking up the banking cartel of fees will require both policy action and consumer vigilance.

Citations And References

All citations in this investigation correspond to verified sources gathered during extensive research across multiple continents and databases. Full documentation available upon email to support the accuracy and verifiability of all claims made.

About Our Investigative Services

Seeking to expose corruption, track illicit financial flows, or investigate complex criminal networks? Our specialized investigative journalism agency has proven expertise in following money trails, documenting human rights violations, and revealing the connections between organized crime and corporate malfeasance across the world and beyond.

Partner With Us for Impactful Change

Our investigative expertise and deep industry networks have exposed billion-dollar corruption schemes and influenced policy reform across Americas and beyond.

Whether you’re a government agency seeking independent analysis, a corporation requiring risk assessment and due diligence, or a development organization needing evidence-based research, our team delivers results that matter.

Join our exclusive network of premium subscribers for early access to groundbreaking investigations, or contribute your expertise through our paid contributor program that reaches decision-makers across the continent.

For organizations committed to transparency and reform, we also offer strategic partnership opportunities and targeted advertising placements that align with our mission.

Uncover unparalleled strategic insights by joining our paid contributor program, subscribing to one of our premium plans, advertising with us, or reaching out to discuss how our media relations and agency services can elevate your brand’s presence and impact in the marketplace.

Contact us today to explore how our investigative intelligence can advance your objectives and create lasting impact.

Read all investigative stories About Businesses And Industries.

* For full transparency, a list of all our sister news brands can be found here.